Jan

2025

Don’t throw away the upside potential of Edinburgh Worldwide’s exciting portfolio

DIY Investor

25 January 2025

Saba Capital’s (Saba) requisitioned meeting to oust the existing board and install two of its own nominees in its place is scheduled for 14 February. However small your shareholding, make sure you vote. Saba has built up a significant stake to force through its agenda while carefully avoiding breaching the limit at which it would have to bid for the whole company. This vote could be decided on the slimmest of margins

VOTE EARLY – if you hold your shares through a platform, the window to vote could be quite small, with some expected to refuse instructions given after 6 February.

Also, to secure the trust’s future, it is important to ensure that you VOTE AGAINST Saba’s proposals and VOTE FOR the AGM resolutions.

Details on how to vote can be found at https://www.trustewit.com/

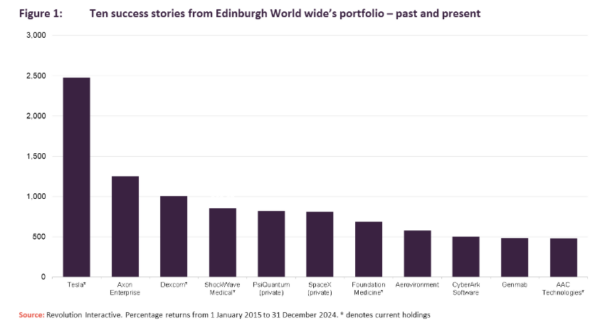

Early access to hidden gems

Edinburgh Worldwide aims to give investors early access to what it describes as “hidden gems, ground-breaking businesses which in many cases are not available on the public markets”. Today, the portfolio offers exposure to themes such as the burgeoning space economy, gene-silencing and sequencing, quantum computing, the fight against cancer, cyber security, high-powered lasers, and rare earths.

The manager’s brief is to identify and back the leading companies of tomorrow, and, as we show in Figure 1 (using a chart taken from the circular issued by the trust) despite battling adverse economic headwinds in recent years, it has demonstrated just how powerful that can be, generating many multiples of returns on investment across a number of companies.

Ignore Saba’s attempt to focus on a short-term setback

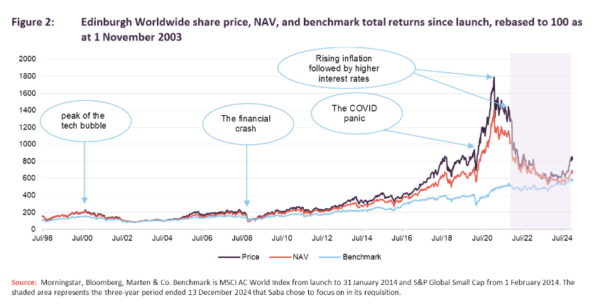

Figure 2 shows Edinburgh Worldwide’s returns since launch, while the shaded area in Figure 1 shows the period that Saba is trying to get you to focus on. The chart has been rebased to 100 as at 1 November 2003 as that was the date that Baillie Gifford took on responsibility for its management.

The upside after a setback can be significant

Since launch, Edinburgh Worldwide has survived a number of challenging periods when market sentiment was against its investment approach. Saba has highlighted one of these, roughly the three-year period since interest rates started to rise in response to rising inflation. Valuations of fast-growing companies tend to be hit in such circumstances. However, the good ones will still thrive and while there will always be some failures, overall, valuations will recover and eventually surpass previous peaks.

For example, between May 2008 and November 2008, Edinburgh Worldwide’s NAV and share price returns fell by around 60%, compared to a 34% fall in its benchmark index (then the MSCI AC World Index). It was another two years before the trust’s NAV recovered to May 2008’s levels, but it soared past that, returning around 250% between the low point and the end of January 2014, when after shareholders gave their approval, the investment approach shifted to investing in small (sub $5bn market cap) companies. Over the same period, the benchmark returned ‘just’ 100%.

This time around, Edinburgh Worldwide’s NAV is already recovering, up 17.8% over the past six months (data from Morningstar to close of business on 21 January 2025), but is still less than half where it was at the peak. Cashing in the portfolio now would kill any hope of further recovery.

The existing board has taken decisive action

Contrary to suggestions by Saba, the existing Edinburgh Worldwide board has been proactive. It already identified areas where it felt improvements needed to be made and has implemented solutions:

- Douglas Brodie, who has managed the portfolio since it adopted its small cap remit, will now have two co-managers, Luke Ward and Svetlana Viteva;

- exposure to loss-making, cash consumptive businesses has been reduced, and the trust now has a better-balanced portfolio with stronger sales and earnings growth;

- the portfolio is more focused; and

- the upper limit on market cap at the time of investment has been lifted, to reflect the shifts in markets since 2014.

In addition, in recognition of the need to tackle an overly wide discount, the board committed to return £130m of capital to investors over the course of 2025.

If you were focused on the discount rather than the potential NAV upside, you’re probably out already

Saba’s aggressive stake-building, in an attempt to build a position large enough to force through its agenda, has driven down the discount. Those shareholders who were frustrated with Edinburgh Worldwide’s short-term returns have been able to sell out. We believe that the overwhelming majority of the trust’s remaining investors will be loathe to hand over control to Saba and lose the latent upside in the portfolio (which could be many, many times the few percentage points that the recent discount narrowing has added), but EVERY VOTE WILL COUNT.

Saba’s main aim is to build its management fee income

Saba says its new board members would sack Baillie Gifford and appoint it as manager. It would then sell off the existing portfolio and invest instead in a portfolio of other investment trusts, aiming to buy them on discounts and then go after them as it has done with its first seven targets, including Edinburgh Worldwide. We are not convinced of the upside from such an approach. It will not help that Saba’s management fees seem likely to be a lot higher than those charged by Baillie Gifford (its closed end fund strategy charges management fees of 1.1% and ongoing charges are a lot higher than that. By contrast, all-in, Edinburgh Worldwide’s ongoing charges are 0.7%).

However, as Edinburgh Worldwide has highlighted in the circular convening the requisitioned meeting, the evidence of Saba’s actions in the US closed end market would suggest that it uses client money to build up significant voting power in targeted trusts, awards itself lucrative management contracts, and then sells down its funds’ exposure again, leaving the minority shareholders who did not get out funding extra revenues for Saba.

Saba lacks experience of the types of unlisted investment held by the trust

We are concerned about the potential for value destruction when Saba attempts to sell off the trust’s unlisted investments. Edinburgh Worldwide’s exposure to exciting businesses such as SpaceX came about because of Baillie Gifford’s extensive team of specialist investors in these types of structures. Saba does not have that depth of resource, or the expertise needed to negotiate profitable exits. Were Saba simply to sell off the trust’s liquid listed investments, the portfolio could quickly become imbalanced.

Serious corporate governance concerns with Saba’s proposal

We are concerned about the prospect of poor corporate governance if the job of looking after your interests as shareholders is handed from an entirely independent board of six directors to two individuals nominated by Saba, one of which is a Saba employee and who could end up on more boards than he could reasonably devote sufficient time to, and neither of which has any experience of being a director of a UK-listed company. Even if that reduced board of two then recruits additional directors, Saba’s statements suggest that it is confident that they will do its bidding.

Why take a leap in the dark?

In addition, we observe that the terms, size, and timing of “liquidity events” that Saba suggests will be forthcoming, are not defined in its requisition. Also missing is any information on its long-term track record. Edinburgh Worldwide’s shareholders are being asked to take a leap in the dark.

Quick buck? or lucrative recovery?

At its heart, this is a choice between taking a small, short-term gain in exchange for an uncertain future, and the potential for a much more lucrative long-term recovery in the trust’s fortunes.

![]() Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this article on Edinburgh Worldwide Investment Trust Plc.

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this article on Edinburgh Worldwide Investment Trust Plc.

Leave a Reply

You must be logged in to post a comment.