Jun

2022

How can investors in resources respond to climate warnings?

DIY Investor

4 June 2022

This year has brought stark warnings over the devastating impacts climate change could have. We look at what this means for investing in resources such as food, water and energy – by Felix Odey

Pressure on the global food and water system is growing as a result of climate change, and time to address its potentially disastrous consequences is running out.

Fresh warnings on rising global temperature are emerging with increasing frequency. For example, the World Meteorological Organization recently estimated that Earth has an almost 50% likelihood of temporarily crossing the crucial 1.5ºC climate change threshold before 2026.

Meanwhile, the most recent report from the Intergovernmental Panel on Climate Change (IPCC) made it clear that we are already seeing irreversible impacts from climate change. It also highlighted that without significant and immediate action, across all sectors and countries, the consequences are likely to be catastrophic.

The rapid phase-out of coal and methane emissions is needed, so too a massive ramp-up in capital investment in transitioning to a low carbon world, and carbon sequestration and reforestation. Without this action we will see rapidly rising sea levels, more extreme weather events, habitat loss, and worsening shocks to the world’s food supply.

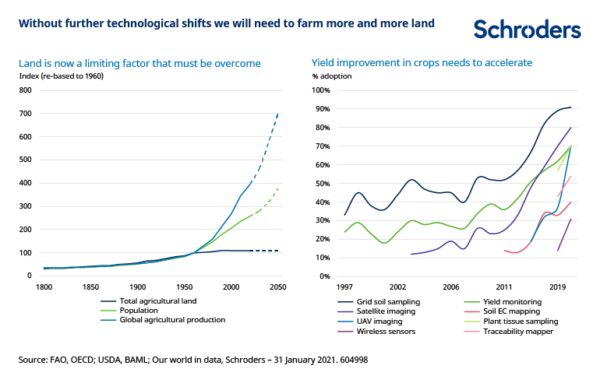

Over 40% of the world’s population is “highly vulnerable” to climate change, according to the IPCC. The global population is expected to exceed 10 billion by 2050, which will require producing 70% more food and water compared to 2010 levels (Source: FAO, USDA, OECD, Our World in Data), and a similar ramp-up in energy consumption.

How we get there, and, specifically, the changes we make in the next decade, will shape the world profoundly.

Nature-based solutions and technology will play a crucial role

A key point from the IPCC report is that we need to stop thinking about climate change as an isolated problem that can be solved by just offsetting or lowering carbon emissions. The global environment is inherently interlinked, and wider land usage is a key variable.

Climate modelling assumptions made by the IPCC, and similar organisations, factor in certain land usage, and natural carbon stabilisation from ecosystems like peatlands, forests and the oceans. Natural environmental stabilisers are being destroyed at an alarming rate, and are approaching a tipping point where negative feedback loops will cause these essential natural resources to degrade irreparably.

Food production accounts for 25% of greenhouse gas emissions, 65% of freshwater usage, and 40% of land usage, according to FAO, with food production often happening near to or even using key stabilising ecosystems, such as the ocean or rainforests. The IPCC emphasises that we need company practices to not only minimise the environmental damage they inflict, but actually encourage the recovery of these natural assets.

If the food system adopted certain land use practices it would be hugely beneficial for climate change mitigation. Such practices include intercropping (growing more than one crop in close proximity), using winter cover crops to encourage soils with greater organic content, and increasing organic inputs.

Forestry and biofuels are also increasingly being used to offset or replace carbon emissions from the energy and transport system. Both of these will put further strain on land use and the natural stabilisers if not managed correctly. This highlights the importance of nature-based solutions and technologies that can improve the yield and resource efficiency of how we produce essential things like food and energy.

What role do investors play?

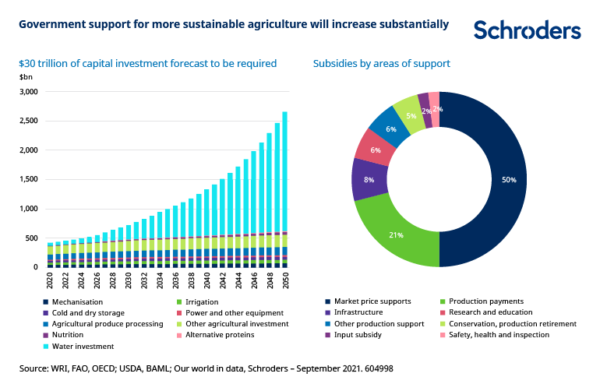

Changes to the energy transition, food, and water value chains are going to involve a huge reallocation of capital; upwards of $130 trillion over the next 30 years based on BNEF, WRI and UN estimates. Traditionally, this kind of capital shift has catalysed share price performance in companies successfully generating returns from higher capital expenditure.

We see multiple drivers and sources of this capital, and the IPCC report highlights that we need the solutions and drivers of change to be as wide-reaching as the problems we face.

But the solution for investors is not as simple as divestment from certain companies, or taking one or two token positions in “ESG champions”. This is a multi-decade trend that will be widespread and will require an investment perspective that manages the nuances within, and interconnections between, the most influential constituent subsectors of the changing systems.

As investors in both food & water and energy transition themes, we aim to follow a three pillar approach to sustainability:

- 1) Create a universe of potential investee companies that covers the whole value chain in these thematic areas, while remaining focused on the problem these investments are trying to help solve;

- 2) Company by company ESG and sustainability analysis, to ensure that we differentiate companies on how they operate as well as their business purpose;

- 3) Engagement, with both the incumbent companies and those offering the products and services we need.

Another core message of the IPCC report is that we must avoid “maladaptation” that has negative unintended consequences.

Instead, the report advocates policy, and investment, that encourages companies to manage the whole range of stakeholder needs and outcomes, including social justice. The United Nations’ Sustainable Development Goals offer a tangible way of assessing which companies are balancing wider environmental objectives with important social objectives.

The IPCC report offers a timely warning to the perils of inactivity, and makes it clear that we have only seen the very beginning of the change that is required across systems like energy, food, and water. Overall, investment in agriculture and land sectors are going to have to increase by three to six times versus current levels in order for climate change to be effectively mitigated.

Investors, companies, governments and organisations like the IPCC need to ensure that data, capital and regulation are aligned to efficiently drive the changes we need before they become even more burdensome and difficult to make.

![]()

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.