Jan

2025

Kings of the castle

DIY Investor

10 January 2025

We reveal the winners of our 2025 Trust Ratings…by Thomas McMahon

We all know there are dangers in relying too much on past performance when picking an investment. Nonetheless, our best and most important piece of evidence when it comes to judging a manager’s skill and the potential of a strategy is how it has done in real, live market conditions. Our quantitative ratings are designed to give a superior assessment of past performance, highlighting the best performers when considering risk, the area of investment and the objectives. We look back over five years of performance, aiming to cover a variety of market conditions, and consider a number of performance characteristics that we think are important to investors. We assess performance against a benchmark chosen quantitatively and within peer groups we have selected to give a fair comparison. Our ratings reward the 20 outstanding performers for growth and for income and growth, as well as highlighting the most successful alternative income trusts. The ratings are purely quantitative, meaning the largest asset managers and boutiques are treated alike, and no commercial interests can interfere. Below we reveal the winners for 2025 in the Growth, Income and Alternative Income categories.

2025 Growth rating winners

Let’s get right to the winners for 2025 – if you’d like to review how last year’s picks did, see lower down. For the Growth rating, we start with an assessment of total return, considering risk-adjusted performance (using the information ratio) and downside risk (using the upside / downside capture ratio). For the Income rating, we then apply some tests to find those that have met yield and dividend growth benchmarks while performing well on a total return basis. We have renamed the Income rating this year from Income & Growth in the interest of clarity, but the calculation remains identical. If a trust qualifies for both awards, we give it the one that we think most accurately reflects its objectives and how it is likely to perform in the future. (For a step-by-step walk-through of our methodology, see appendix.)

Our system is designed to recognise a variety of strategies rather than simply produce a list of those trusts that have been helped the most by whatever style has been in favour over the past five years. As such, we think the fact the average Growth / Value score of the twenty Growth rating winners for 2025 is almost perfectly neutral at 0.3, on a scale of 5 to -5, is some indication of success. It is interesting that on average the trusts with a greater tilt to value have a higher Quality score, which may reflect the fact that quality has been a better-performing factor than value. Both stylistic scores are our own creations, using a number of fields in Morningstar and applying a simple algorithm.

New Growth rating winners for 2025 include AVI Japan Opportunity (AJOT) and Vietnam Enterprise Investments (VEIL). We think it is worth flagging that Fidelity China Special Situations (FCSS) has again achieved a rating, despite its market suffering a torrid time. FCSS has done very well at limiting its exposure to the Chinese market’s downside and capturing the upside, and this has contributed to positive five-year performance while the Chinese market is down.

2025 Income rating winners

There are four trusts winning an Income rating this year, all of which have an enhanced yield, paying a fixed amount of NAV out as a dividend. Our ratings require trusts to have delivered on average 3% dividend growth over the past five years. The potential drawback with enhanced dividends is that if the NAV falls year-on-year, the dividend may fall too. Our ratings suggest that over the medium term, this doesn’t have to get in the way of providing attractive dividend growth. We note that one other rating winner, Montanaro UK Smaller Companies (MTU), has also switched to an enhanced dividend policy, starting in 2025.

It is notable to see Aberforth Smaller Companies (ASL) win a rating this year. ASL is one of the few unabashedly ‘value’ equity strategies left in the investment trust sector, and has performed extremely well post-pandemic. Its strong performance on dividend growth and very high revenue reserves qualify it for an Income rating. It joins a number of UK small-cap trusts on the list this year. We think this reflects the deep value in the sector, with a historically successful growth market providing all sorts of companies with a handsome yield – and increasingly buybacks too.

We think it is interesting to note the average Quality score of the Income rating winners is higher than the Growth rating winners (at 6.2 to 5.4). There are a couple of reasons this might be the case. First, it may reflect the fact that high quality earnings and dividend growth performance are intrinsically linked. Secondly, it is also true that our ratings value good downside performance, as we think that investors value this highly and it more reflects their understanding of risk than volatility. It is by design that a trust that delivered a return of X% annualised and dividend growth of Y% would score higher if the path of returns were steadier and saw more modest drawdowns, and a trust that had a much more volatile path to the same result would have a lower score. Finally, we would note that our style scores are all relative to the funds’ peers. As such, a Quality score over 5 means a score above average for the relevant investment trusts, not in relation to the underlying equity market. We believe the average quality score of the investment trust sector would be above that of the market, with quality being an important factor for many managers.

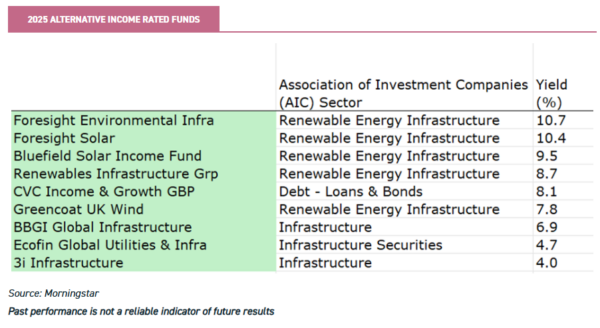

2025 Alternative Income rating winners

For the first time, the number of Alternative Income rated funds has fallen, reflecting the impact of an interest rate shock on the valuations of unlisted portfolios, financing costs and net cash yields. For this rating, we look across the relevant sectors for those trusts that have managed to deliver a flat or stable NAV along with dividend growth over the past five years. Only nine made the cut this time, down from 14 last year. The two battery storage funds that qualified in 2024 are among those dropping off. All our calculations are on NAV, not share price, and wide discounts on some of these trusts suggests investors may be wary of these NAVs too. On the other hand, stalwarts and early movers Greencoat UK Wind (UKW), Renewables Infrastructure Group (TRIG) and BBGI Global Infrastructure (BBGI) have navigated through the turmoil to retain their ratings in 2025. As can be seen in the table below, the solar funds are on particularly wide discounts, which is reflected in the very high yields on offer in the table below.

We don’t apply a minimum yield requirement for these ratings, but they are formulated to focus on those portfolios designed to deliver a high income. Notably there is still a substantial yield pickup over gilts available from most of the trusts on our list, which reflects in part discounts. In fact, we tend to think it is this that is driving the discounts, rather than wariness of the NAVs, which interpretation may increase the attractiveness of the cheap share prices.

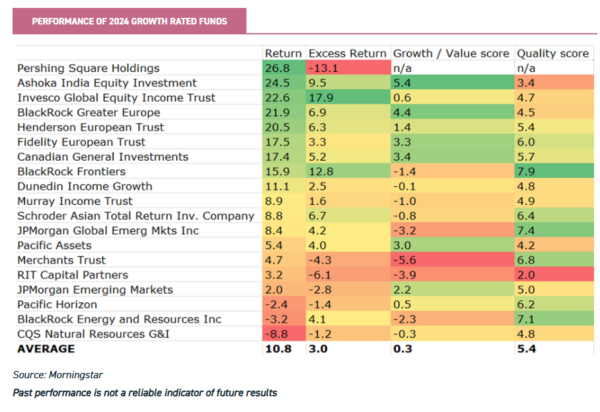

Performance of 2024 rated funds

The tables below show how our rated funds for 2024 did. As ever, we warn that we view one year as being too short a period to make judgements about a strategy. Nonetheless, it is interesting to see how the picks performed. The growth funds outperformed the income and growth funds, reflecting the outperformance of the growth factor over the period. There were no specialist technology funds to have won a rating, reflecting the fact that while their absolute performance was excellent, relative to their indices they didn’t stand out. However, Pershing Square Holdings’ (PSH) collection of US large-cap growth stocks saw it lead the list, while Ashoka India Equity (AIE) delivered another strong year in absolute terms and relative to the Indian market. It is worth noting that to fairly reward good active management, performance is measured against a benchmark picked via correlation analysis, and style-specific benchmarks are included. As such, Invesco Global Equity Income (IGET) performed extremely well versus a high dividend yield index, reflecting the managers’ ability to deliver a high and growing income plus attractive growth.

The best-performing Income & Growth rated fund over 2024 was JPMorgan Global Growth & Income (JGGI). JGGI has one of the strongest growth tilts of those to have won an Income & Growth rating, a function of its enhanced dividend policy that sees it pay a dividend largely from capital. It is perhaps more surprising given the backdrop to see TR Property (TRY) as one of the very best performers. Its strong NAV returns reflect a recovery in real estate that we think may have slipped under the radar as investor attention was elsewhere.

The outstanding performer from the 2024 Alternative Income rated funds was high yield credit fund CVC Income & Growth (CVCG). The company currently offers a high yield of 8.1% despite trading at par. There are higher yields on offer from others in the list, and some exceptionally wide discounts. As discussed above, this may represent scepticism about the NAVs of some of those investing in unlisted assets. As the return column shows, there weren’t many write-downs of portfolio values over 2024, and discounts generally remain wide.

Conclusion

We think the investment trust sector tends to attract the best managers; the structure gives managers plenty of flexibility to generate alpha, while the closed-ended nature means the management contracts are highly prized by fund groups. Boards can take advantage of the high level of competition for those contracts to incentivise managers. Our ratings recognise those managers who have done particularly well to generate outperformance and mitigate the market risk during a highly volatile period over the past five years.

Appendix: Our methodology

To identify the top growth trusts, we start by looking at performance versus the benchmark. For us, the information ratio is the key metric. This looks at the outperformance of a fund versus an appropriate benchmark and then relates this to the extent of divergence from the benchmark or the extra risk taken. In other words, it seeks to identify whether the active risk relative to the benchmark taken by the manager has been rewarded with outperformance. We then look at the performance of a fund in rising markets versus its performance in falling markets – the upside/downside capture ratio. We think this has two attractions. The first is that it reflects the ‘loss aversion’ of the average investor. Behavioural finance teaches us that investors prize avoiding loss more than they do achieving a quantitatively equivalent gain. This is captured by an upside/downside capture ratio above one, which means that the fund has a tendency to avoid losses by a more significant degree than it makes gains in rising markets. The second attraction is that it allows us to consider defensive and aggressive strategies on a more level playing field. A trust that does exceptionally well in rising markets and is level in falling markets could rank the same as a trust that protects very well in falling markets but only keeps up in rising markets.

In order to create fair comparisons between funds, we have divided our universe into ‘super sectors’ of asset classes: large- and mid-cap equity funds, small-cap funds, fixed income, or equivalent funds and property funds. This is intended to reflect the fact that generating alpha, in particular, is much easier in small-caps, so comparing small-cap managers with large-cap managers is unfair. It also overlooks the risks that small-caps bring, such as volatility and illiquidity, which means that it is not inherently superior to large-cap investing despite the advantages with regard to alpha. We rank trusts within their ‘super sector’ on all quantitative metrics. In order to reward persistence, we review performance over a five-year time period, which makes it much harder for a single year to distort results. We also exclude trusts that have had a management change in the past three years.

It perhaps goes without saying that all our analysis is based on NAV total return performance, which reflects the strategy and decisions made by the manager, rather than share price, which can reflect many other factors. As already discussed, we would never envisage such a rating being used on its own to determine investment decisions. Clearly, with investment trusts, the discount of the shares to NAV and the policies and the quality of the board all need to be considered too. As importantly, given that quantitative studies are backward-looking, investors need to make a judgement about the likelihood of past performance patterns persisting in ever-changing markets. By looking over a long time period, we hope to capture a broader set of market conditions, but some trends last for much longer than five years.

For our Income ratings, we start with the screens used for the Growth ratings. We then look at current yield and dividend growth, over five years. To win the rating, a trust needs to have a 3% yield and 3% per annum dividend growth over the past five years as a minimum, allowing for high-yielding funds and dividend-growth funds to be considered together. Once we have screened out the trusts that don’t meet the yield and dividend-growth tests, we order the trusts by their quantitative score on our growth screens. We apply the same manager tenure screen. We do sense check the quantitative results and will jump in if we think an exception needs to be made, but our threshold for doing so is exceptionally high, as our intention is to present the numbers, not our opinions.

We also present an Alternative Income rating in order to analyse the top performers in this relatively new and rapidly growing space. We think, for the most part, trusts in the infrastructure, renewables and related sectors are held for a stable and high income, most likely by those living off their income. High yield is likely more important than income growth. We have developed a simple screen showing those trusts that have at least maintained their NAV and their dividend, in nominal terms, over the past five years. With the alternative income space being relatively young, there are not many trusts with a long track record and just applying these two screens whittles the space down considerably.

Disclaimer

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Leave a Reply

You must be logged in to post a comment.