Apr

2024

Quarterly Markets Review – Q1 2024

DIY Investor

6 April 2024

A look back at markets in Q1 when global equities posted robust gains

The quarter in summary:

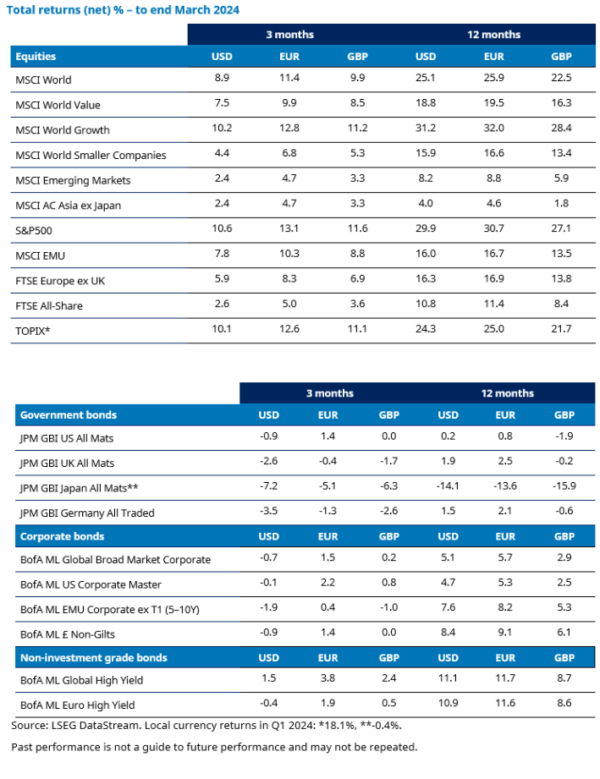

Global stock markets registered strong gains in Q1 amid a resilient US economy and ongoing enthusiasm around Artificial Intelligence. Expectations of interest rate cuts also boosted shares although the pace of cuts is likely to be slower than the market had hoped for at the turn of the year. Bonds saw negative returns in the quarter.

Please note any past performance mentioned is not a guide to future performance and may not be repeated. The sectors, securities, regions and countries shown are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

US

US shares registered a robust advance in the quarter. Gains were supported by some well-received corporate earnings as well as ongoing expectations of rate cuts later this year. The pace of monetary policy easing is likely to be slower than had been expected at the end of last year, given resilient US economic data, but this did little to dampen appetite for equities.

The S&P 500 index was boosted by good corporate earnings, including from some of the so-called “Magnificent Seven” companies. Gains were led by the communication services, energy, information technology and financials sectors. Real estate registered a negative return while utilities also lagged.

The Federal Reserve (Fed) kept interest rates on hold at 5.25-5.5%. US inflation ticked up slightly to 2.5% year-on-year in February, from 2.4% in January (as measured by the personal consumption expenditure metric). Fed chair Jerome Powell said that the central bank will be “careful” about the decision on when to cut rates. The latest “dot plot” that details policymakers’ expectations of rate cuts suggests three cuts this year.

Data releases generally demonstrated ongoing economic resilience. Annualised GDP growth for Q4 was revised up in the third estimate to 3.4%. Nonfarm payrolls were robust although the unemployment rate rose in February. The ISM manufacturing PMI signalled expansion after 16 straight months of contraction, rising to 50.3 in March.

Presidential primaries were held in several states during the quarter. Donald Trump is the presumptive nominee of the Republican Party while his main challenger Nikki Haley dropped out of the race in March.

Eurozone

Eurozone shares posted a strong gain in Q1. The information technology sector led the charge amid ongoing optimism over demand for AI-related technologies. Other top gaining sectors included financials, consumer discretionary and industrials. Improvements in the economic outlook boosted more economically sensitive stocks while banks were supported by some announcements of improvements to shareholder returns. By contrast, utilities, consumer staples and real estate were the main laggards.

Over the quarter there were signs of improving business activity in the eurozone. The flash eurozone purchasing managers’ index (PMI) rose to 49.9 in March compared to 49.2 in February. This signals that business activity is almost at stable levels. (PMI data is based on surveys of companies in the manufacturing and service sectors. A reading above 50 indicates growth while below 50 indicates contraction).

Eurozone inflation continued to cool in the quarter. The annual inflation rate (consumer price index) was 2.6% in February, down from 2.8% in January. In February, European Central Bank President Christine Lagarde sought to downplay the chances of an imminent interest rate cut. She told the European Parliament that the central bank does not want to run the risk of reversing any cuts.

UK

UK equities rose over the quarter. Financials, industrials and the energy sector outperformed, along with some of the other economically sensitive areas of the market. Market expectations moved to price in a sooner-than-expected first UK interest rate cut as inflation undershot the Bank of England’s (BoE) forecasts.

At the end of the period the BoE’s Monetary Policy Committee (MPC) decided at its March meeting to keep the UK’s main policy interest rate on hold at 5.25%. Annual inflation, as measured by the consumer price index, has fallen from a peak of 11.1% in October 2022 to 3.4% in February, the lowest rate of price increases since September 2021.

Meanwhile, official data showed that the economy had entered a technical recession in the second half of 2023. This occurred as the tailwind of post-pandemic “revenge spending” came to an end and the headwinds of higher inflation and interest rates weighed on activity. The market reaction to the Spring Budget was largely muted, possibly suggesting that investors had anticipated a bolder budget.

Overseas inbound bid activity for smaller and mid-sized UK quoted companies remained an important theme over the period.

Japan

The Japanese equity market experienced an exceptionally strong rally, with the TOPIX Total Return index recording a total return of 18.1% in Japanese yen terms. During the quarter, foreign investors played a leading role in driving the rally. This was fuelled by increasing optimism over Japan’s positive economic cycle, characterised by mild inflation and wage growth. This quarter marked a historic moment as the Nikkei reached its all=time high and surpassed the 40,000 yen level. The Bank of Japan (BOJ) also took significant actions at its March policy meeting, contributing to the new high for the Nikkei 225.

The market’s performance has been driven by large-cap stocks, particularly value stocks in sectors such as automotive and financials. Additionally, the global boom in artificial intelligence (AI) and semiconductors has also contributed to the rise in stock prices of semiconductor-related companies. On the other hand, domestic and defensive sectors, including land transportation, services, food, and pharmaceuticals, have lagged.

Corporate earnings in Japan have exceeded expectations, and there have been positive revisions for both the current and the next fiscal years. The weakening yen has provided support, but more importantly, the inflationary environment is expected to boost earnings for many Japanese companies, especially those with pricing power (the ability to raise prices by more than inflation).

The BOJ’s decision to overhaul its monetary policy measures, including lifting the negative interest rate policy, abandoning yield curve control (YCC), and ceasing the ETF purchase programme, was supported by the significant progress made in the spring wage negotiations known as Shunto. The initial figures released by the unions exceeded 5%, surpassing the previous year’s levels and reaching a 34-year high.

The BOJ set a short-term rate at 0.0-0.1%, indicating a shift to a positive policy rate, rather than just zero. This demonstrated the BOJ Governor Ueda’s strong confidence in Japan’s macroeconomic development. At the same time, the BOJ committed to maintaining its accommodative policy stance, providing some comfort to the currency market and leading to further weakening of the Japanese yen.

Asia (ex Japan)

Asia ex Japan equities achieved modest gains in the first quarter, with share prices bouncing back from recent lows and investors displaying cautious optimism that the gloom surrounding China may be starting to lift. Taiwan, India, and the Philippines were the strongest markets in the MSCI AC Asia ex Japan Index while Hong Kong, Thailand, and China ended the quarter in negative territory. Stocks in Taiwan achieved strong growth in the quarter, driven by on-going investor enthusiasm for AI-related stocks and technology companies.

Despite rallying somewhat in the middle of the quarter, Chinese stocks still ended the quarter modestly lower as foreign investors remain cautious amid ongoing fears about the outlook for the Chinese economy. Stocks in Hong Kong also experienced sharp declines in the first quarter, with many investors looking to other markets as Beijing increases its control over the former British colony and amid ongoing fears over the state of China’s post-pandemic economic recovery.

Indian stocks also performed well in the first quarter with investors hopeful that the political stability that has unpinned India’s recent stock market growth will continue if Narendra Modi wins a third electoral victory this year. India has gained from overseas investment in manufacturing as companies seek to diversify supply chains outside of China, while the country’s physical and digital infrastructure has also improved.

Emerging markets

Emerging market (EM) equities gained over Q1 2024 but underperformed compared to developed market peers. China dragged on returns despite some select policy stimulus measures. A delay in expectations about the timing of Federal Reserve (Fed) interest rate cuts aided returns but negatively impacted interest rate sensitive markets such as Brazil.

Peru was the top-performing index market, aided by currency and monetary policy easing measures including a reduction in the country’s reference rate to 6.5% and a lowering of the reserve requirement ratio for local currency deposits. Turkey also posted strong returns as the central bank continued its orthodox monetary policy approach by increasing interest rates over the quarter, most recently with a surprise 500bps hike at its March 2024 meeting. The Colombian index market also benefited from monetary policy developments as the central bank lowered interest rates to 12.75% in January and to 12.25% in March.

Index heavyweight Taiwan outperformed strongly on the back of continued investor enthusiasm about artificial intelligence (AI) and the tech sector. January’s presidential election saw the ruling Democratic Progressive Party (DPP) remain in power but lose its majority in parliament, which markets took well as it makes the continuation of the status quo more likely. India also outperformed, helped by local currency strength ahead of April’s general election, in which incumbent Prime Minister Modi seeks a third term.

Korea posted a positive return but underperformed broader EMs due to weakness in speculative AI and battery stocks. China fell in US dollar terms, dragged down by returns in the healthcare sector in particular. Ongoing US-China tension, most recently in the form of attempts by US lawmakers to discourage investments into China, also weighed on sentiment in the quarter. South Africa was another poor performer against a backdrop of political uncertainty in the run-up to 29 May’s general election while Brazil underperformed on profit-taking after the market’s strong performance in 2023. Egypt generated the worst returns over the quarter on the back of its c. 35% currency devaluation.

Global bonds

The first quarter of 2024 saw a significant shift in the landscape of inflation and interest rate expectations. Initially, the market anticipated faster central bank action to lower interest rates. However, expectations were scaled back, with notable exceptions including the Bank of Japan (BoJ), which increased interest rates from -0.1% to 0.1% for the first time in 17 years, signalling an end to negative rates. Meanwhile, the Swiss National Bank surprised the markets with a 25 basis point cut to 1.5%. The European Central Bank, the Bank of England, and the Federal Reserve (Fed) all proceeded with caution, avoiding premature declarations of victory over inflation.

Global economic activity was on the upswing. The US economy continued to outperform, buoyed by sustained consumer spending, thanks to rising real wages amidst easing inflation. Although the eurozone’s progress was slower, there was reason for optimism with a rebound in the service sector and manufacturing showing signs of revival. China’s recovery also continued, although the property sector continued to struggle.

Inflation remained a central concern for markets. Despite indications of diminishing inflationary pressures, unexpected high inflation readings tempered enthusiasm for imminent rate cuts. Both the US and eurozone reported inflation rates exceeding forecasts, raising alarms about the enduring nature of service sector inflation.

As the quarter progressed, governmental bond yields adjusted in response to shifting market sentiments and economic indicators. 10-year government bond yields increased across the board (meaning prices fell). The US 10-year Treasury jumped from 3.87% at the end of Q4 2023 to 4.21% at the end of Q1 2024. The UK 10-year gilt yield rose from 3.54% to 3.94%, while the German 10-year Bund yield steadied at 2.03% – a 26 basis point increase from the end of Q4. Corporate bonds surpassed government bonds in performance with UK high yield as a notable outperformer. Investment grade bonds are the highest quality bonds as determined by a credit rating agency; high yield bonds are more speculative, with a credit rating below investment grade.

Convertible bonds did not fully benefit from the strong equity market tailwind. The FTSE Global Focus convertible bond index advanced a mere 1.1% in USD hedged terms for the quarter. Primary market activity remained strong with a good level of demand for new convertibles coming to the market. The current state of refinancing activity in the convertible market can be characterised as opportunistic. Companies are not displaying a sense of urgency to tap into the convertible market for liquidity. Valuations, however, remain subdued.

Commodities

The S&P GSCI Index achieved robust growth in the first quarter, with all components of the index ending the period in positive territory. Energy and livestock were the best-performing components, while agriculture and industrial metals achieved more modest growth. Within energy, all sub-sectors achieved strong price growth apart from natural gas, which experienced a sharp price fall in the quarter.

Within agriculture, the price of cocoa rocketed higher in the quarter due to strong demand and shortages in West Africa, where more than half of the world’s cocoa beans are harvested. In industrial metals, zinc and aluminium prices fell in the quarter, while prices for copper, lead and nickel were modestly higher. Both gold and silver prices also advanced in the first quarter.

Digital assets

After a slow January, digital asset markets took off in February and March resulting in one of the strongest quarters in recent history. Bitcoin and Ethereum returned 68.8% and 59.9%, respectively. Bitcoin reached a new all-time high on 14 March.

These strong returns were generated in a supportive macro environment and high demand following the approval and subsequent launch of eleven physically backed Bitcoin ETFs (exchange traded funds) in the US on 11 January. These products have seen net inflows of $12.1 billion since inception.

Market dynamics have also seen a step-change since last quarter, with Bitcoin trading volumes up 85% year-to-date. There continue to be lower correlations between digital assets while correlation to traditional risk assets, such as equities, remains low.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

![]()

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Leave a Reply

You must be logged in to post a comment.