Feb

2024

Monthly markets review – January 2024

DIY Investor

8 February 2024

A review of markets in January, when equities saw mixed performance and hopes of imminent US rate cuts were dashed at month end.

The month in summary:

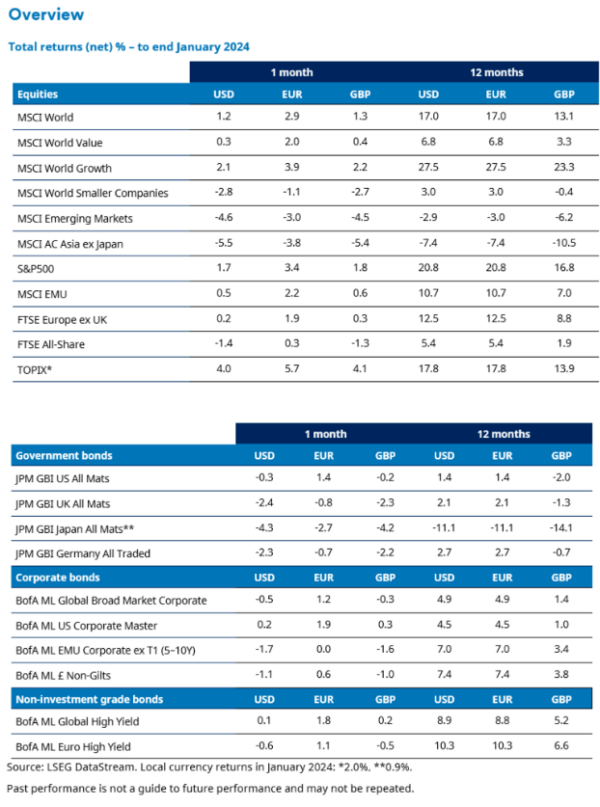

Stock markets were mixed in January with developed market shares advancing while emerging markets saw negative returns. There were signals from major central banks that interest rate cuts may not be forthcoming as soon as had been hoped. In bond markets, government bond yields rose (meaning prices fell). Oil prices moved up amid ongoing conflict in the Middle East and disruption to shipping.

Please note any past performance mentioned is not a guide to future performance and may not be repeated. The sectors, securities, regions and countries shown are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

US

US shares advanced in January, supported by some strong corporate earnings and data suggesting a soft landing for the economy will be achieved. Hopes of imminent rate cuts also boosted shares, although such hopes were dashed by the Federal Reserve (Fed) at month end.

Communication services and information technology were the strongest sectors in January, supported by robust earnings and positive outlook statements from some of the “Magnificent Seven” large cap companies. By contrast, real estate and materials were among the weakest sectors.

Data showed that US GDP grew at an annualised rate of 3.3% in Q4 2023. For the year as a whole, GDP growth was 3.1%. Meanwhile, annual inflation (as measured by the consumer price index) ticked up to 3.4% from 3.1%. Labour market data remained firm with non-farm payrolls showing 216k jobs added in December and the unemployment rate steady at 3.7%. The ISM manufacturing (PMI) remained in contraction but ticked up to 49.1 from 47.1 in December (a reading above 50 for the PMIs – purchasing managers’ indices – indicated expansion, while below 50 implies contraction).

The Fed held a policy-setting meeting at the end of the month. Interest rates were kept on hold, as expected, at 5.25-5.5%. Comments from Fed chair Jerome Powell indicated that, while rates have peaked, a rate cut as soon as the next meeting in March is unlikely.

Eurozone

Eurozone shares posted a gain in January, led higher by shares in the information technology (IT) sector. The communication services sector also performed strongly. Sectors that had rallied in late 2023 on hopes of imminent rate cuts – including utilities and real estate – were among the weaker performers.

In the IT sector, shares of some semiconductor equipment stocks registered robust gains. While the sector faces a ban on the export of some high-end chipmaking equipment to China, demand elsewhere remains high. The software subsector also performed well.

Hopes of an early interest rate cut from the European Central Bank (ECB) began to fade after inflation (as measured by the consumer price index) for December was confirmed at 2.9%, up from 2.4% in November. However, inflation eased again in January with the flash estimate at 2.8% y/y. The ECB kept interest rates unchanged at its January meeting. However, rate cuts are still expected to come later in the year. ECB president Christine Lagarde said that “the disinflation process is at work”.

The eurozone economy registered zero GDP growth in Q4 2023. This followed a -0.1% contraction in Q3. This mean annual GDP growth for the single currency bloc was 0.5% in 2023. The German economy was the main drag on growth, shrinking -0.3% in Q4.

UK

UK equities fell over the month as expectations for when interest rates may begin to be cut were pushed out. This occurred following an unanticipated increase in UK inflation as the Office for National Statistics (ONS) revealed that the consumer prices index had increased to 4.0% in December, from 3.9% in November.

The consumer inflation numbers added to a complicated picture for UK macroeconomic data, with other statistics from the ONS revealing the wage growth had slowed in the three months to November. Meanwhile, the statistics agency also revealed that UK economy had performed better than expected in November.

Chancellor of the Exchequer Jeremy Hunt hinted he would announce major tax cuts in the upcoming spring budget. Against these developments and the increased geopolitical uncertainty, the market struggled to make progress, with the large UK-quoted diversified energy and basic materials firms and financials underperforming.

The technology, consumer discretionary, consumer staple and healthcare sectors outperformed. Overseas inbound bid activity for smaller companies remained an important theme over the period, further helping to underpin performance of the UK small and md-sized companies as overseas buyers made further approaches.

Japan

The Japanese equity market enjoyed a strong start of 2024 with a total return of 7.8% for the TOPIX index in January. The Nikkei 225 surged by 8.4%, reflecting the fact that the market rise was driven by large cap stocks. Foreign investors led the rally on expectations of structural changes in Japan, including the launch of the new NISA (Nippon Individual Savings Account) for Japanese retail investors.

Japan began the new year with two disasters: an earthquake in the Noto region on 1 January and a terrible accident at Tokyo Haneda airport on 2 January. However, the economic effects of these events are expected to be relatively minor. The market responded positively upon opening from 4 January, reaching a new post-bubble high intra-month. This is partly due to renewed expectations of a policy change by the Bank of Japan (BOJ) in light of the earthquake.

As expected, the BOJ did not make any policy change at its January meeting. The currency market reacted to this development, with the Japanese yen depreciating. This depreciation further boosted the stock market, as a weaker yen benefits exporters’ earnings.

As a result, value stocks including automotive, trading companies, banks, and securities companies, rose strongly whereas domestic oriented and defensive stocks lagged.

The highlight of January was that the Tokyo Stock Exchange (TSE) announced the list of companies which responded to their request for management plans considering cost of capital and stock prices. Market participants saw this as an important step in Japan’s corporate governance reforms. It provides a clearer picture of the policy’s development as well as further pressure on corporate management, given that TSE will update the list every month. According to TSE, c.40% of listed companies have already disclosed plans.

The October-December quarterly earnings results started to be released late the month. The numbers were encouraging although some technology companies downgraded their earnings estimates.

Asia (ex Japan)

Asia ex Japan equities fell in January as investors scaled back their expectations for swift interest rates cuts and amid ongoing concerns about weaker economic growth in China. China, Hong Kong, and South Korea were the weakest index markets in the month, while India and the Philippines achieved modest gains.

The sell-off in China comes amid investor concern that the world’s second-largest economy could face a long period of slow economic growth, with factory output contracting for the fourth consecutive month in January. The crisis in China’s property market, once the engine of economic growth, also continues to weaken investor sentiment towards the county’s stock market.

Share prices in Thailand and Singapore were also significantly lower in the month, while declines recorded in Taiwan, Malaysia and Indonesia were more modest. In contrast, India achieved a modest gain in the month with the country’s stock market continuing to attract strong inflows from overseas investors as well as domestic participants, reflecting its growing strategic status as an alternative to China.

Emerging markets

Emerging market (EM) equities declined in US dollar terms in the first month of 2024, underperforming developed markets which finished the month in positive territory. China was once again the main drag on performance. Concerns that the Federal Reserve (Fed) will keep rates higher-for-longer added to the negative sentiment in EM amid signs of economic strength in the US.

Chile posted the biggest losses in the month with weakness in the peso weighing on returns. Difficulties at a major lithium producer, which saw it temporarily stop extraction activities amid community protests, also had a negative impact. China was another significant underperformer in January as a bigger-than-expected reduction in the reserve requirement ratio failed to lift markets against a backdrop of the ongoing property crisis which saw the indebted property giant Evergrande liquidated. There was also news of further US sanctions on Chinese technology companies. The Korean market, which is typically sensitive to the outlook for US interest rates, also lagged the index.

Thailand underperformed, amplified by local currency weakness, as did Czech Republic. In Brazil, underperformance came despite relatively resilient macroeconomic data and a cut to the central bank’s policy rate to 11.25%. In South Africa, the rand weakened along with the prices of major industrials and precious metals.

Poland outperformed despite delivering a negative return in US dollar terms. Similarly, Peru and Mexico were down but performed better than the index. Peruvian authorities lowered the country’s reference rate for the fifth time in as many months, this time to 6.5%. Mexico’s outperformance was underpinned by returns from financial companies. Taiwan did better than the index, helped by the technology sector. January’s presidential election saw the ruling Democratic Progressive Party (DPP) remain in power and the previous vice president Lai Ching-te voted in as president. The DPP lost its majority in parliament, which markets took well as it makes the continuation of the status quo more likely. Saudi Arabia and the UAE also outperformed, with strength in energy prices beneficial for both markets.

The remaining markets generated positive returns, including Colombia where the central bank cut interest rates by 25bps to 12.75%. In India, local demand for equities boosted the market while in Hungary, optimism about the speed at which the central bank could cut rates helped returns. Kuwait and Turkey both gained, with the latter raising rates to 45% and signalling the end of the hiking cycle.

Global bonds

In January, global government bond markets saw a partial reversal in the positive performance experienced at the end of 2023. Despite encouraging news on disinflation, the enthusiasm for near-term rate cuts subsided as the US economy continued to demonstrate robust growth.

Yields rose across all major government bond markets, meaning prices fell, with the UK 10-year rising from 3.54% to 3.80%. German 10-year yields also moved higher from 2.03% at the end of December to 2.16% and peripheral spreads tightened. US Treasuries fared better with the 10-year yield rising from 3.87% to 3.95%.

Investment grade (IG) corporate bonds posted negative returns, yet they still outperformed government bonds with new issuance being absorbed well and spreads tightening further on the hopes of a soft landing. Within high yield, the eurozone was the notable outperformer, with tighter spreads and positive total returns which exceed its investment grade counterparts. Investment grade bonds are the highest quality bonds as determined by a credit rating agency; high yield bonds are more speculative, with a credit rating below investment grade.

From a macroeconomic perspective, the theme was one of ongoing regional divergence. The US economy sustained its momentum, with Q4 GDP surpassing expectations (4.9% against a forecast of 2.0%) and the composite purchasing managers’ index (PMI) for January climbing further into expansionary territory, reaching its highest level since June. By contrast, the eurozone’s growth remained lacklustre. This sluggishness was underscored by a disappointing German Ifo Index – typically a reliable growth indicator – which unexpectedly fell in January. Additionally, consumer confidence has also dipped across the region.

Inflation pressures continued to ease. The Federal Open Market Committee’s (FOMC) preferred measure, core PCE inflation, softened to 2.9% year-on-year in December, inching closer to the Federal Reserve’s (Fed) 2% target.

In light of the swift shift in market expectations towards rate cuts that transpired late last year, investors closely monitored central bank meetings for signs of any pushback against this stance. The European Central Bank maintained rates, but the overarching tone of the meeting was more dovish than anticipated, noting progress on inflation. The FOMC met on the last day of the month, with Powell’s comments during the press conference, seemingly raising the bar for the first rate cut to be delivered as early as March, needing to see greater confidence that “inflation is moving sustainably towards 2%.”

The dollar rebounded versus its G10 peers as investors scaled back their aggressive expectations for rate cuts. The Japanese yen was the underperformer, reversing some of the previous month’s gains.

Commodities

The S&P GSCI Index rose in January with strong price gains for livestock and energy offsetting weaker prices in agriculture, industrial metals, and precious metals. Oil prices rose amid ongoing conflict in the Middle East and disruption to shipping in the Suez canal.

Industrial metals was the worst-performing component of the index in January, with price gains for lead and copper prices failing to offset price falls for aluminium, nickel, and zinc. Within agriculture, sugar and cocoa prices advanced sharply, while prices for wheat, corn and soybeans fell. In precious metals, gold and silver prices were both lower in the month.

Digital assets

Digital asset markets were mixed in January. Bitcoin and Etherem returned +0.4% and -0.2% respectively, with Altcoins giving back some of last quarter’s outperformance.

The month began with the much anticipated SEC approval of a spot Bitcoin ETF (exchange-traded fund) which has seen nearly $1.5 billion in net inflows so far. This is an important milestone in the institutionalisation of the asset class.

For the first time, US investors have a regulated and straightforward way to gain exposure to Bitcoin through a traditional brokerage account. This eliminates the need for setting up crypto wallets or navigating cryptocurrency exchanges, making Bitcoin more accessible to a wider audience of investors in the same way the gold ETF did in the early 2000s.

After Bitcoin, the spotlight turns to Ethereum, the second largest digital asset. Many asset managers have filed to list an ETH ETF, with initial expectations for approval as early as May this year.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

![]()

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Alternative investments Commentary » Commentary » Equities » Equities Commentary » Equities Latest » Exchange traded products Commentary » Fixed income Commentary » Fixed income Latest » Latest » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.