May

2022

Returns from Structured Products

DIY Investor

25 May 2022

The rules that govern structured products are many and varied so it is vital that you understand the terms of any product you may be considering before you sign on the dotted; you could be agreeing to tie your money up for up to six years and if you do get it wrong, you may find it difficult to redeem the product or you may be forced to do so at a considerable loss by Christian Leeming

The return you receive is usually based on the performance of an index, often the FTSE 100, although sometimes plans base their returns on a basket of shares.

Deposit and investment based structured products generally pay their returns on one of three ways:

- Kick out plans – each product runs for a set period of time, generally five or six years but have the potential to mature early, or ‘kick out’, if an index has risen at a certain date or dates, usually the plan anniversary. If the index has risen and the plan kicks out the product comes to an end and the initial capital is repaid along with interest for each year that the plan has been held (see example below).

- Defined return plans – provide a ‘defined return’ if certain conditions are met; for example if at the end of the plan term a specified index has risen, then capital will be repaid plus a pre defined interest payment.

- Variable return plans – these provide a return linked to the total return of a specified index or basket of shares over the term of the plan. Sometimes these returns are ‘geared’ for example a plan may provide a return of 200% of the rise in the FTSE 100 over the term of the plan with a specified cap, perhaps 50%.

The conditions are usually checked on each anniversary of each plan’s start date and it may kick out if its conditions have been met; often, the plan has a minimum term of two years, so the conditions are only checked from the second anniversary onwards.

If the conditions that would trigger a kick out are not met and the product reaches the end of its term, your initial investment will usually be returned with no gain.

If the index to which the product is linked falls below a particular level – often 50% of its initial level – you may lose some of your capital and if it were to continue to fall, your losses would be pro rata to the decline in the level of the index.

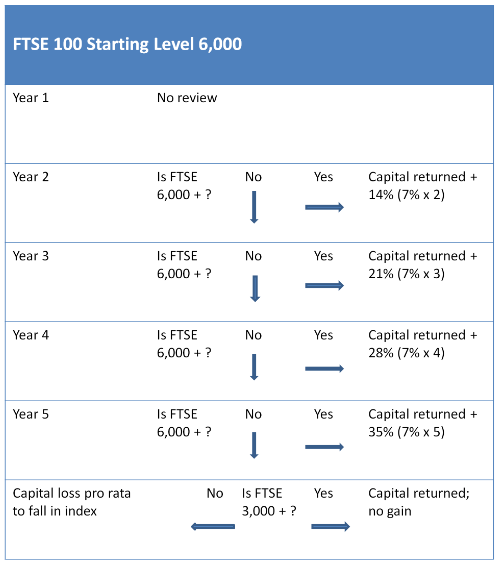

Example of a structured investment based upon the FTSE 100 with a starting value of 6,000, with a minimum term of two years; the value is checked each year from the second anniversary and, in this instance, pays 7% for each year that the product is held until kick out or maturity.

If the products kicks out, your payment represents the number of years x 7%; if the index has not reached 6,000 yet is above 3,000, you get your money back with no bonus.

If the FTSE is below 3,000 (50% of its starting value) you will lose some of your capital pro rated to the fall in the index.

Leave a Reply

You must be logged in to post a comment.