Jul

2023

The Changing Face of Emerging Markets

DIY Investor

6 July 2023

The Changing Face of Emerging Markets – part II, Addressing your feedback – By Mark Martyrossian, Director, Head of Distribution, Aubrey Capital Management

Rob Brewis published a piece a couple of weeks ago on the evolution of Emerging Markets (“EM”). Although EM indices play no part in our process, their changing constituents do reflect the development of the underlying economies.

Rob’s piece stirred a certain amount of feedback which centred on the risk/reward characteristics of the universe. On balance, we believe that the broadening of the asset class and the smaller proportion of cyclical stocks is a good thing for investors.

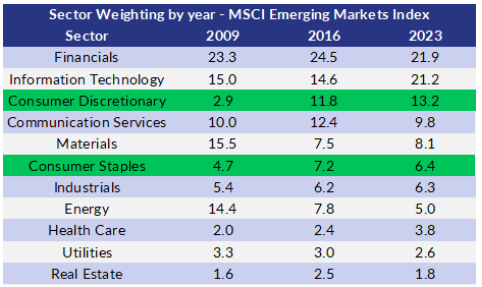

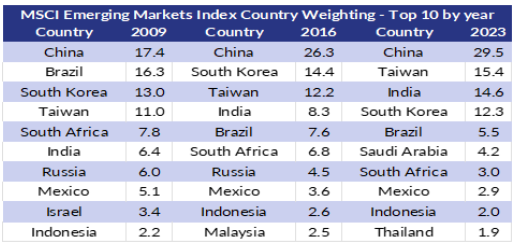

The following tables show the sector and country constituents, ‘Then’ (2009 and 2016) and ‘Now’. This is a reference piece more than anything else, with answers to some of the client feedback we received on Rob’s original.

The growing importance of the consumer and the declining significance of energy and materials are both big positives in our view: more secular, less cyclical pure and simple. Our premise, as you know, is that the growth of the EM consumer is the optimal way of tapping into the positive top-down characteristics of EM.

After all, it is the exciting demographics that attracts investors, so why squander the opportunity by chasing stocks that march to a global cyclical beat (energy, materials etc.) or have significant state ownership.

Given that consumer stocks are now a bigger proportion of the Index (consumer discretionary and consumer staples have gone from being 7.6% of the Index in 2009, to 19.6% in 2023, highlighted above), it could be said that the market is “coming to us.”

This prompted several of you to ask whether we would now face greater competition for the best consumer names. We are relaxed about this – despite being an All-Cap strategy, our active share is high, ranging between 85% and 95% since inception in 2012.

So, the prospect of ETFs and more index-driven funds piling into consumer names that are in the Index is not a worry.

Many of you have asked how we manage to avoid the likes of South Africa, Turkey and Russia. Being bottom-up stock pickers, our fundamental analytics very often do the country selection for us.

Quite simply, there are better stocks elsewhere. We have companies from South Africa and Turkey on our Watchlist, but they have not figured in our portfolio for several years. They just did not make the cut.

We are however ‘macro-aware’ meaning that a fundamental change in the top-down of a particular country may well see stocks on our Watchlist get promoted into the Focus List and thence to the portfolio.

This happened in India at the end of 2013. It is important to stress that this macro awareness is not a top-down bet. As mentioned, we are bottom-up stock pickers, so an improving macro can increase our confidence in our forecasts but is not in and of itself a reason for increasing exposure to a country.

Finally, as you know, South Korea’s status as an emerging economy has once more been in the news. This has been a long running saga – well over a decade according to my memory. And yet again, following the recent MSCI review, it has failed to make the graduation to Developed Market status.

The South Korean consumer sector is not the richest of hunting grounds for us but such a graduation if/when successful will require a redistribution of the weighting (currently 12.3%) amongst the remaining 23 countries in the Index.

A PDF version of this article is available here

Alternative investments Commentary » Alternative investments Latest » Brokers Commentary » Commentary » Equities Commentary » Equities Latest » Exchange traded products Commentary » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.