May

2023

Investing Basics: What are Synthetic ETFs for?

DIY Investor

6 May 2023

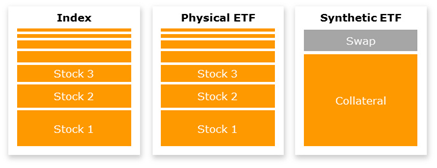

You would expect an index tracker to actually invest in the same holdings as its index. This is how a physical ETF works and why it returns the same results as the market it mimics By Christian Leeming

But synthetic ETFs don’t work this way often because the markets they track are very hard to physically recreate at a reasonable cost; a market may consist of many small and illiquid securities that are very expensive to trade or complexities of tax, time zones and local laws may make it difficult to track some global indices.

How a synthetic ETF replicates its index

In the case of commodities it would be inconceivable to take delivery of thousands of cows because you wanted to track livestock so a synthetic ETF uses a total return swap instead of physical holdings to earn the return of its index.

A total return swap is a derivative contract provided by a counterparty such as a global bank or other large financial institution whereby the counterparty pays the ETF the return of the index it tracks including dividends in exchange for a fee and the investment return of collateral posted on behalf of the ETF.

Collateral is used to mitigate the possibility of investors losing out if the counterparty defaults on its obligation to pay, which exposes synthetic ETFs to some counterparty risk which investors should understand.

Cash invested in the ETF secures a basket of securities that form its collateral, and this would be sold and the proceeds used to return the investor’s money if the counterparty were to default.

Collateral is often held in securities completely unrelated to the market the ETF follows – a FTSE All-Share synthetic ETF may hold some of its collateral in bonds or Japanese equities!

UCITS ETFs (those approved and regulated by EU rules) are not allowed to expose more than 10% of their Net Asset Value (NAV) to counterparty risk and many providers apply even stricter criteria and ‘over collateralise’ so that the ETF is protected by collateral worth more than 100% of its NAV.

Synthetic ETFs have been subject to a great deal of scrutiny from the media and regulators which has led providers to spread the risk by using multiple counterparties, increase the quality of collateral and revalue it daily in order to ensure that it is 100% of NAV, thereby reducing counterparty risk.

Synthetic ETFs have two main advantages over physical versions.

Firstly, synthetics provide a low cost way to access certain niche markets that would otherwise be off-limits to most investors.

Secondly, they can sometimes undercut their physical rivals in certain markets with lower Ongoing Charge Figures (OCFs) and tracking error because they avoid the complexities of trading the securities of the index.

Your broker should allow you to screen the products on its platform by replication method, or you can use the Screener at www.justetf.com.

Exchange traded products Commentary » Exchange traded products Latest » Financial Education » Latest

Leave a Reply

You must be logged in to post a comment.