May

2022

Why bother investing? The power of compounding

DIY Investor

19 May 2022

![]()

This blog is especially important for younger readers

I fancy working on an easy blog after a few recent ones where I have had to use my brain – there are plenty of more interesting things going on than the stockmarket and all its accoutrements.

Someone asked me to do a blog on how much money you might need to give up work; I have been thinking about how to write this one and got distracted quite a bit, but I reckon I have the shape in my mind now. However, in order to write that blog, I need to write this one first – i.e, I am still ducking the request!

‘the power of compounding to show how money can grow at various different annual percentage growth rates’

What I want to do here is to take an example amount of cash and use the power of compounding to show how money can grow at various different annual percentage growth rates. In combination with this I will address what are realistic returns – and this ties back to an earlier WheelieBlog I did called the ‘Rule of 72’ which you can read here:

http://wheeliedealer.weebly.com/blog/the-rule-of-72-and-its-implications-on-our-expectations

The maths

I will take an amount of cash and multiply it by a percentage annual return (PAR); I will then take the result and multiply that by the same PAR etc etc.

This sequence should show how the starting amount of cash grows over time according to the Compound Annual % Growth Rate – CAGR.

The parameters of the calculations

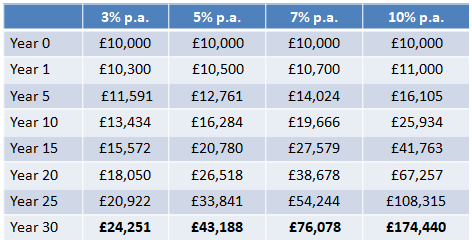

I will start with £10,000 – an arbitrary figure but an amount that people can relate to. I understand these numbers are commutative – so if you have £100,000 as your starting point, then you just add a ‘0’ onto the numbers (i.e. multiply by 10). If your starting point is £40,000, then just multiply by 4; if your Starting Point is £5,000, then halve the numbers – you get the point.

The Annual Growth Percentages I will use are as follows:

3% – This would be a very good return on cash at the moment.

5% – Nice round number.

7% – Real returns (after inflation) for the stock market over many years are around this kind of number. In theory, you could get this from index tracker funds – although not easy with costs.

10% – The kind of return I aim for on the exposure value of my portfolio. I am sure many great investors and traders achieve more than this – but it takes effort and I am happy to have an easy life and not trade all that often.

12% – A bit of safe leverage on a portfolio should make this possible – but far from easy.

15% – This is an extremely good return few people can achieve.

20% – An exceptional rate of return! – Buffett probably only just gets near. Robbie Burns does better than this but he is extremely unusual.

Please note, I am totally ignoring inflation for ease and simplicity; there may also be some very slight rounding errors – I have tended to round down.

Tax is not included and the growth percentages chosen include dividends – i.e. when I say 7% growth, part of that is achieved from dividend payments. It therefore follows that if you buy stocks without dividends then you are setting yourself behind from the start – you’d better be confident of your expectations of fast capital growth.

30 years seems a sensible number to choose, and the figures are for the end of each year.

5% – Big number that isn’t it? Bet you didn’t expect it to be so much bigger than the result for 3%. Note that just 2% difference has such an impact when returns are compounded over 30 years – and consider what this means if you have Costs of 2% a year.

7% – In a similar way to the previous example, that just a couple of % from 5% to 7% makes a huge difference to the Overall Return after 30 years – almost doubling it.

10% – Wow, the jump there is amazing – just 3% more (OK, in reality that is a lot!) and the final figure is way over double.

At 12% £10,000 turned into £300,000; 12% is difficult to achieve, especially in the early years whilst you are learning, but it is not impossible with some leverage. I am quite shocked by the outcome. The higher percentages to come are more for fun really (few people will be able to achieve this) – the numbers will be bonkers

Well, I said it would be a big number – 15% returns £662k and 20% almost £2.4m – Now that is a huge number! You can see why Warren Buffett is so loaded.

Tax

All of these calculations have no allowance for tax; you may object that this is unrealistic (or even immoral – if you believe that governments spend your money well), but I think it is on the basis that £10,000 is well below the current ISA limit for one year and leaving your money to grow in such a tax avoidance (legal) wrapper is just good sense.

There is a risk that future governments could change the ISA rules and there is talk that a limit of £1m could be put on the value of money you can have in an ISA – I guess the theory is that they would tax anything above the limit and this could hit the returns in the tables above.

The government has reduced the lifetime limit on SIPPs to £1.25m, but with careful use of SIPPs, ISAs, spread bets, Capital Gains Tax Allowance and Personal Income Tax Allowances, many tax implications can be reduced.

Portfolio Management Costs

It should be clear to you that just a couple of % changes from one table to another have a massive difference on the final returns created. Likewise it is vitally important to minimise your costs of running your portfolio – keeping platform costs as small as possible as well as dealing fees and buy/sell spreads where possible.

Tools such as magazines, tipping websites, software for trading are all real costs and should be minimised as much as you can.

As an example, let’s say you have a portfolio worth £100,000 and you expect to invest for another 20 years and you are a pretty shrewd investor and expect to achieve a 10% return.

In this case, if you can save 1% on costs in Year 1 – i.e. £1000, over the 20 years this is £6725 extra return. (I worked this out by knocking a Zero off the £10,000 starting figure and dividing the 20 year figure by 10). Obviously such savings in the following years will boost returns considerably rather than eating away at your gains.

‘if you are an Old Git like me it has less impact, but for anyone below 30 these numbers are immense’

If you have £100 of unnecessary cost in Year 1 and you are achieving 12% returns per year on average, then this will add up to £2995 over 30 Years!; you can apply this logic to your wider spending of normal life – every £100 you p*ss away on lager could really be costing you £2995!

This is why it is critical to control every aspect of your spending and to realise that if you can just save a few hundred pounds per year, it has a massive impact over time. I appreciate that if you are an Old Git like me it has less impact, but for anyone below 30 these numbers are immense. Mind you, even for an Old Bug*er, £100 over 10 years at 12% could be costing £310.

All that money people have wasted on Lottery Tickets over the years……..what a con that is; taxing the dreamers…….I have never done the Lottery (I find it pretty distasteful) and I like to think that I have WON thousands and thousands of quids by not wasting my money on it. In addition, I have then gone on to invest that money I did not waste by investing it at good rates of return.

You must avoid mistakes

You will hopefully now see the importance of having realistic expectations of what you can achieve and how vital it is to ensure you are not taking avoidable risks. I think it is realistic for an individual committed long term investor to aim for 10% CAGR per year but it is very hard to achieve this in practice.

It sounds easy, and many of you will have done much better than this over many years recently but most of us underestimate the damaging effects of the odd bad year. If you have been steadily achieving 10% CAGR for say 6 years, and then you get hit 30% in a horrible bear market, you will then be massively behind the game.

One horrific year can have terrible consequences, so it is better to not be greedy and to aim for steady, tortoise like returns over many years and to avoid the really big pullbacks – this is all about risk management and avoiding high risk gambles.

It is better to avoiding downside risk than to try to pick big winners

This is vital for those in your 20s, 30s., but still Important for all of us; I would be considerably wealthier now if I had not lost lots of money in my early years as an investor. I was a bit unlucky because I started investing at the top of the dotcom boom – I don’t think this was necessarily greed although that probably played a part. It was more that I happened to have a pile of cash and needed to do something with it.

‘I lost something like 40% of my portfolio in a few years’

The consequence was that I lost something like 40% of my portfolio in a few years and it is obvious from the tables above how much this hurt me. Luckily I had the good sense (probably pure luck really) to diversify with some bonds and cash etc. but it set me back many many years.

The only thing I got right was that I did not give up and I made big efforts to learn what I was doing!

Avoid mistakes in your early years as they have such a huge impact later

Of course, this is hard to do as, by definition, in your early years you are younger and less experienced, and therefore more prone to screw ups. You must use resources like the WheelieDealer Website and other stuff from experienced investors to help you avoid mistakes; reading Robbie Burn’s Naked Trader book is essential.

I wish the WheelieDealer Website had existed when I started out (anyone for time travel?)

Benchmarking

There has been some recent discussion on Twitter about benchmarks and it has pretty much followed the usual well-trodden path of selecting an index to benchmark your performance against; I have a slightly different slant on this issue as I find this not all that helpful (or necessarily healthy for an investor’s state of mind).

Rather than using a benchmark constructed from an index or a hybrid version based on a couple of indices, maybe it would be better to make your benchmark one of the columns in the table above.

For example, you could decide that you want to achieve 12% CAGR year in year out and you would use this kind of table to track your performance against. You would need to decide your starting cash and any cash you add in over the years would need to be added into your ‘benchmark’ table calculations.

This is more what I do in practice – for me, the problem with benchmarking against an index is that firstly I hold stocks of all sorts of market cap sizes and from various indices and secondly that the weightings I use are completely different to those that make up any indices – so how meaningful is it really to benchmark against an index?

‘how meaningful is it really to benchmark against an index?’

To add colour to this, consider the Nasdaq – something like 14% or so of the index is Apple (AAPL) – how many people have 14% of their portfolio in Apple? Would it be wise to do so anyway? Very few indices are equal weighted to the constituent stocks and they will not be the same as the wightings in your portfolio. It really is questionable how useful such benchmarks are.

There is a fair argument to say, well, if you can’t beat 7% CAGR each year (which is pretty much what the FTSE100 would probably give you if you bought a low cost tracker fund), then what is the point of investing in individual stocks?

However, this perfectly logical point misses an important element for me – I actually ENJOY my investing activities and just owning a tracker fund would be utterly unfulfilling for me from a personal achievement point of view (I guess it’s something to do with the ‘Self Actualising’ bit of Maslow’s ‘Hierarchy of Needs’!)

I am of the view that I enjoy my investing and the money that flows from it is a secondary thing – and I suggest that this applies to anything in life. If you are enjoying it and passionate about it, you will probably make money from doing it.

By benchmarking against an Index that is made up of strange weightings and that is an approximation at best of your portfolio, you might be setting yourself up to fail. Just as you could probably have a run of good luck and beat your synthesised and imperfect benchmark, you could just as easily under-perform it for unavoidable reasons (that are beyond your control) and this might really knock your confidence as an investor – never a good situation as you need to be calm and rational and not affected by avoidable anxieties.

As ever, it is up to you as an individual to decide what you are happiest with – but maybe the idea of a benchmark based on a CAGR % table might be more useful.

The point of the table is to show how compounding returns over many years can grow your wealth, and how it is vital to avoid unnecessary tax and costs; these kind of tables are a huge help in determining when you can give up work (or reduce the amount of work you do and go part time) and how much you need to invest to achieve your retirement goals.

You could create a similar table to work out how your wealth could grow from, as an example, a buy to let property but it is a lot of hassle and has a lot of hidden costs that can eat away at returns.

Using tables in a practical sense

The first thing to do is to decide how many years you want to work for – for example, if you expect to work another 15 years, then years 0 to 15 of the tables are relevant to you.

Next, you need to decide on a rate of return that you think you can realistically achieve. If you experienced, then probably 10% is sensible and if you are particularly sharp, then 12% may apply. If you are new to the game and quite young, then maybe 7% is more applicable – remember, these numbers are for formulating a rough plan, if you happen to outperform, then that is icing on the gateau.

Then determine your starting point; if you have £50,000, then you can multiply all the numbers by 5 – remember, these things are commutative (I love using that word – I was taught it in maths at junior school and have never ever had need to use it since – so now, 39 years on Dear Reader, I am ramming it down your throat)

‘If you find that the final number you get is lower than you wanted, then you will need to consider working more years’

Just these few parameters from above will give you an idea of the total return after your time period until retirement. However, you can get much more sophisticated by adding money into the fund each year if you think you will be saving more. For instance, you might start with £10,000 and then add in £1000 each year after – this will take some maths and a calculator, but you should be able to work it out.

Remember, these numbers do not include inflation – and it is guesswork anyway. A good way to handle the inflation element, might be to drop down the rate of return tables a bit. For example, if you expect to do 12% a year, then you could drop down to 10% as the 2% difference might be a fair proxy for inflation (I believe that the true average long term inflation rate is about 3% – so you may need to go a bit lower.)

If you find that the final number you get is lower than you wanted, then you will need to consider working more years, finding more money, or maybe how you can achieve a higher rate of return – none of these are easy options.

Anyway, I think that just about covers it. Have fun creating your tables!

Kali bradi, WD

![]()

Commentary » Equities » Equities Commentary » Equities Latest » Financial Education » Take control of your finances commentary

Leave a Reply

You must be logged in to post a comment.